Why countries do not adopt IFRS?

.

Similarly, you may ask, which important country has not adopted IFRS?

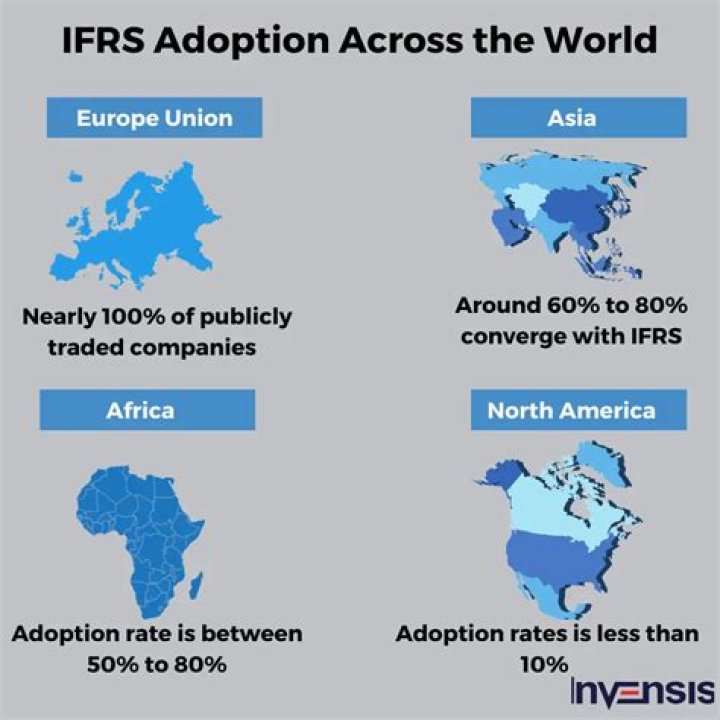

Three jurisdictions (China, India and the United States) account for nearly all (95%) of the GDP of profiled jurisdictions that do not permit the use of IFRS Standards for any domestic publicly accountable entities.

Secondly, how many countries have adopted IFRS? Approximately 120 nations and reporting jurisdictions permit or require IFRS for domestic listed companies, although approximately 90 countries have fully conformed with IFRS as promulgated by the IASB and include a statement acknowledging such conformity in audit reports.

why is there a need to adopt the IFRS?

As a source of globally comparable information, IFRS Standards are also of vital importance to regulators around the world. And IFRS Standards contribute to economic efficiency by helping investors to identify opportunities and risks across the world, thus improving capital allocation.

Why must listed companies comply with IFRS?

IFRS are designed to bring consistency to accounting language, practices and statements, and to help businesses and investors make educated financial analyses and decisions. Companies benefit from the IFRS because investors are more likely to put money into a company if the company's business practices are transparent.

Related Question AnswersWhat is adoption of IFRS?

Adoption of IFRS, in simple terms, means that the Country applying IFRS would be Implementing IFRS in the same manner as issued by the IASB and would be 100% compliant with the guidelines issued by IASB. Thus, Countries converging with IFRS may deviate to a certain extent from the IFRS's as issued by the IASB.What are the benefits of IFRS?

Benefits include improved comparability to other companies in an industry, a possible increased following in the marketplace and more efficiently priced capital. Unfortunately, in cost/benefit analyses of IFRS adoption, benefits are less tangible than costs and more difficult to quantify.Is IFRS difficult?

The IFRS is not a complicated or difficult standards, but it's provide a some specific recognition or measurements criteria to record the transaction in Financial Record/ Statement. When you learned all the standards issued by ICAI then you move towards IFRS.Who use IFRS?

Adoption. IFRS Standards are required in more than 140 jurisdictions and permitted in many parts of the world, including South Korea, Brazil, the European Union, India, Hong Kong, Australia, Malaysia, Pakistan, GCC countries, Russia, Chile, Philippines, South Africa, Singapore and Turkey.Does UK use IFRS?

United Kingdom. All domestic companies whose securities trade in a regulated market are required to use IFRS Standards as adopted by the EU in their consolidated financial statements. Alternatively they may use IFRS as adopted by the EU.Should US companies be allowed to use IFRS?

Domestic public companies must use US GAAP. Permitted. Currently, more than 500 foreign SEC registrants, with a worldwide market capitalisation of US$7 trillion, use IFRS Standards in their US filings. The IFRS for SMEs Standard is neither required nor expressly permitted.Which countries use GAAP?

This book explores differences between International Financial Reporting Standards (IFRS) and US generally accepted accounting principles (US GAAP), as well as differences in accounting practices between countries such as China, France, Germany and Japan.What countries use IFRS GAAP?

IFRS is used in more than 110 countries around the world, including the EU and many Asian and South American countries. GAAP, on the other hand, is only used in the United States. Companies that operate in the U.S. and overseas may have more complexities in their accounting.How many standards are there in IFRS?

The following is the list of IFRS and IAS that issued by International Accounting Standard Board (IASB) in 2019. In 2019, there are 16 IFRS and 29 IAS.What are the main objectives of IFRS?

Its principal objectives are:- to develop, in the public interest, a single set of high quality, understandable, enforceable and globally accepted international financial reporting standards (IFRS Standards) based upon clearly articulated principles.

- to promote the use and rigorous application of those standards;