What type of loan is best for a home addition?

.

In this manner, what type of loan is best for home improvements?

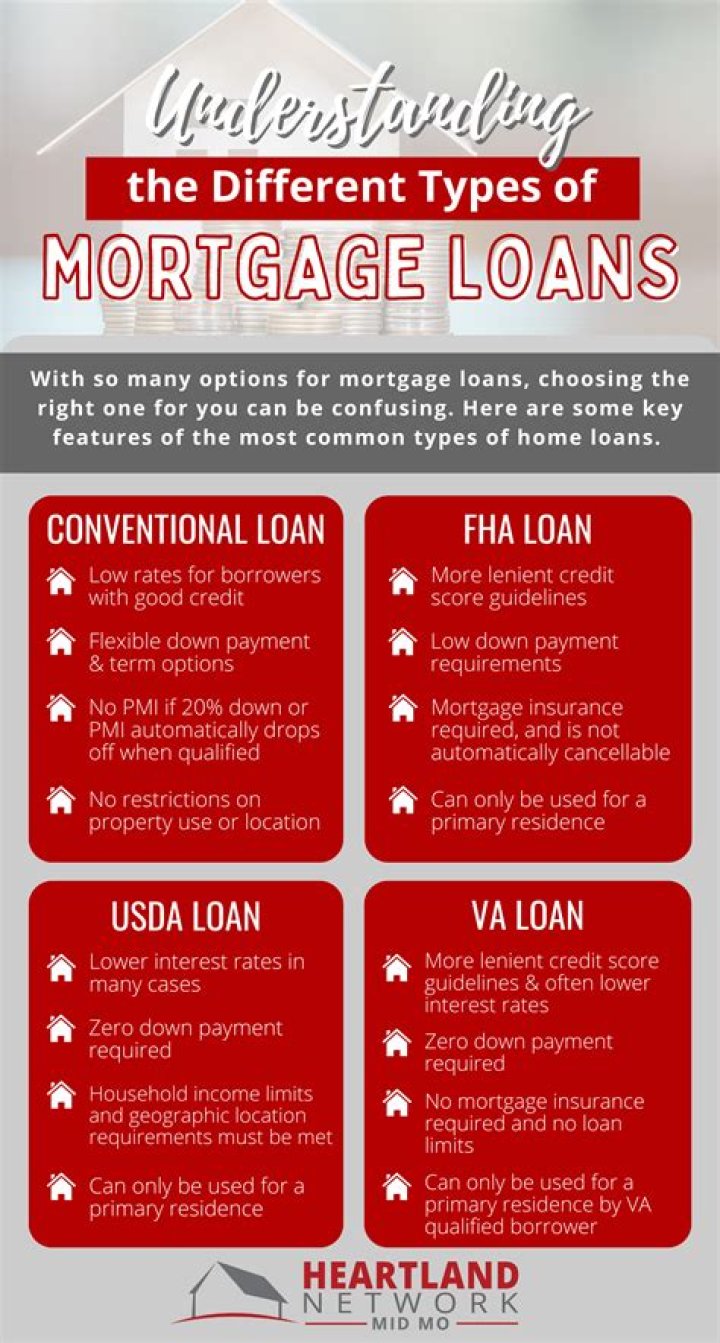

The Best Home Improvement Loans: Summed Up

| Lender | Best APR | Term |

|---|---|---|

| LightStream | 4.99% APR | 2-12 years |

| LendingClub | 6.46% APR | 3 to 5 years |

| Avant | 9.95% APR | 2-12 years |

| Prosper | 6.95% APR | 3-5 years |

Subsequently, question is, can you add a home improvement loan to your mortgage? However, instead of taking out a second mortgage, a cash-out refinance replaces your original mortgage. Your refinanced home loan will have a new balance, payment, interest rate and terms. Government Programs for Home Improvement. Some government programs can help pay for a home remodel.

Besides, how do you borrow money for home addition?

Instead of refinancing your mortgage, this option lets you borrow against the value of your built-up home equity. Rather than paying off your home renovation debt over 30 years, a home equity loan or line of credit gives you a separate monthly bill to cover the costs of your home addition.

What is the difference between a home equity loan and a home improvement loan?

A home equity loan leverages the money you've already paid towards your house—your home equity—as a guarantee to the lender that you'll repay the loan. A home improvement personal loan, on the other hand, is an unsecured loan, so the lender takes on additional risk.

Related Question AnswersDo banks give home improvement loans?

Credit unions, traditional banks and online lenders offer home improvement loans. These are unsecured loans, meaning the homeowner doesn't provide any collateral for the loan. The interest rate will also depend on the borrower's credit score, the loan term and the amount borrowed.What are rates for home improvement loans?

Estimate your home improvement loan rate Interest rates on personal loans generally range from about 6% to 36%. As with most credit products, the rate you receive depends a lot on your credit score. The better your score, the lower your rate and the less interest you'll pay over the life of the loan.What do I need to know about home improvement loans?

Make sure you estimate the cost of your home improvement and the time it takes to pay off the loan. Home Equity products may save money on projects over a shorter period than a cash-out first mortgage. Always consider financing the projects that improve the value of your home.How do you pay for home renovations?

Home Equity Loan or Line of Credit (HELOC) A home equity loan is the classic way to finance home renovations. Take out a loan against the equity in your own house. Lower interest rates than personal loans and credit cards. Large amounts of money may be available for large projects like additions.What happens when you refinance a loan?

Refinancing a loan allows a borrower to replace their current debt obligation with one that has more favorable terms. Through this process, a borrower takes out a new loan to pay off their existing debt, and the terms of the old loan are replaced by the updated agreement.Do home improvement loans work?

A home improvement loan isn't a specific type of loan. In these cases, your home serves as collateral for the money you borrow, and the lender may be able to foreclose on your home if you can't repay the money. Unsecured loans don't require collateral and include personal loans and credit cards.What is the current interest rate on a home equity loan?

5.82%Do I need an architect for a home addition?

Usually homeowners will hire an architect before the contractor is involved. While it might be nice, in most cases hiring the architect who designed the plans to oversee an addition or remodel isn't necessary. So if you're on a budget, it makes more sense to handle dealing with the contractor yourself.Why are home additions so expensive?

The cost of home additions may appear to be way more expensive (per square foot) than the cost of new home construction. Why? Because in a new build, the cost of the most expensive rooms in the house (kitchens and baths) gets spread over double or triple the square footage.How much does it cost to add a 12x12 room?

The average room or house addition costs $86 to $208 per square foot, with most homeowners spending between $22,500 and $74,000. Adding a 20x20 family room costs $48,000 on average, while adding a 12x12 bedroom costs about $17,300.What is the best way to finance home improvements?

Home improvement financing types- Mortgage refinance. If you financed your home a few years ago and your interest rate is higher than current market rates, a mortgage refinance could lower your rate — and your monthly payments.

- Home equity line of credit.

- Home equity loan.

- Personal loan.

- Credit card.

- Save up and pay cash.

Can you increase mortgage for renovations?

Increasing your mortgage for home improvements might add value to your property but using a further advance to pay off debts is rarely a good idea. The additional loan would be linked to your property, which you could lose if you weren't able to keep up your extra loan payments.Can you use a construction loan for an addition?

To pay for large remodeling projects such as this, homeowners often take out a construction or renovation loan, which entails refinancing with a mortgage that reflects the house's estimated value post-remodel. Many lenders provide mortgages that cover up to 80 or 85 percent of the remodeled home's value.What are the disadvantages of home equity loans?

While equity loans often provide lower interest rates than unsecured financing, there are risks and disadvantages.- The Lien. To secure your home equity loan, your lender puts a lien on your property in the same way your original mortgage lender does.

- Monthly Installments.

- Equity Reduction.

- Less Flexibility.