What mortgage company does Dave Ramsey recommend?

.

Also to know is, what kind of mortgage does Dave Ramsey recommend?

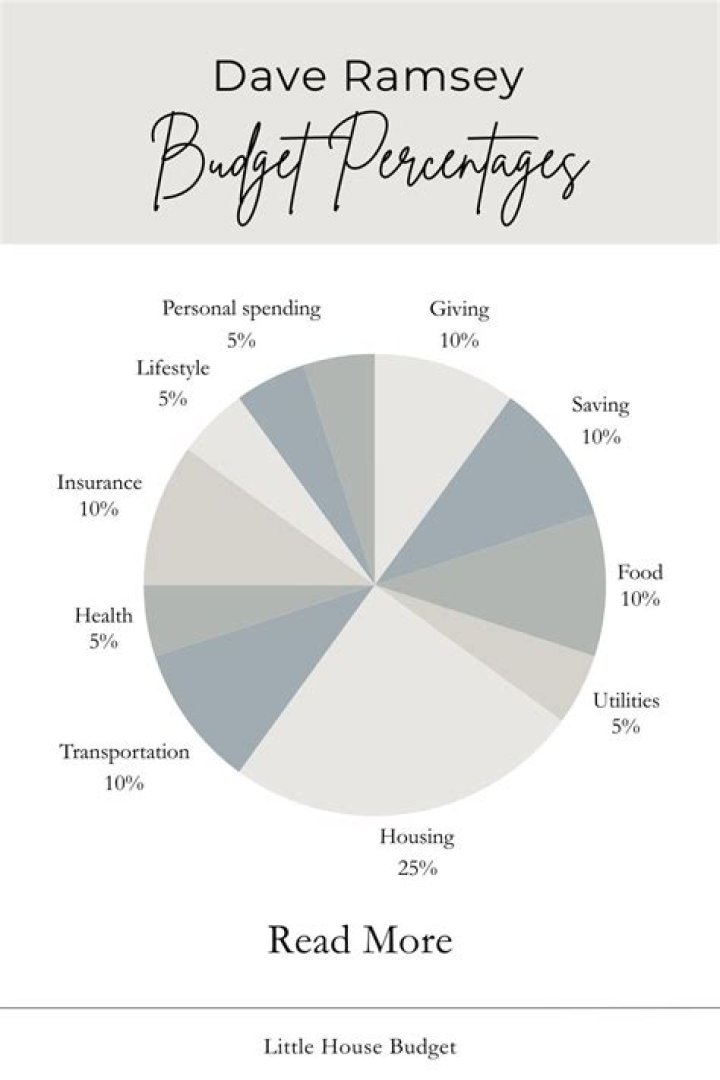

Dave Ramsey recommends your housing payment, including property taxes and insurance, to be no more than 25% of your take-home income. To maximize your savings, you should get a 15-year, fixed rate mortgage. That means the maximum amount John and Jane should spend on their home payment each month is $1,500.

Similarly, who Should I get my mortgage through? Summary of 5 Tips for Finding the Best Mortgage Lenders

| Lender | Minimum Credit Score | Minimum Down Payment |

|---|---|---|

| Chase NerdWallet rating Learn more at Chase | 620 | 3% |

| Quicken Loans NerdWallet rating Learn more at Quicken Loans | 620 | 3% |

| Vylla NerdWallet rating Read review | 620 | 3% |

| Reali Loans NerdWallet rating Learn more at Reali Loans | 620 | 5% |

Also to know, does Dave Ramsey believe in mortgages?

A mortgage is a huge financial commitment, and you should never sign up for something you don't understand! Dave Ramsey recommends one mortgage company. This one! It's likely that your lender will approve you for more money than you want to spend.

What life insurance company does Dave Ramsey recommend?

Zander Insurance

Related Question AnswersWhat does Dave Ramsey say about renting?

The short answer is: Your rent payment should total no more than 25% of your take-home pay. That's the magic number. As mentioned above, your monthly rent should be no more than 25% of your take-home pay.What does Dave Ramsey say about PMI?

Dave says when you're willing to pay PMI. ANSWER: When you're willing to pay PMI. Private mortgage insurance will run $70–75 per month per $100,000 borrowed.How much house can I afford with 50k a year?

Conservatively, your monthly housing costs should total 28% or less of your total gross income. By this measure, a single adult with a $50,000 annual salary, or $4,167 in gross pay per month, can pay housing costs of up to $1,167 per month.Should I use a bank or mortgage company?

Mortgage companies sell the servicing. Unlike a mortgage “broker,” the mortgage company still closes and funds the loan directly. Because these companies only service mortgage loans, they can streamline their process much better than a bank. This is a great advantage, meaning your loan can close quicker.How do you know your budget for buying a house?

To determine how much house you can afford, most financial advisers agree that people should spend no more than 28 percent of their gross monthly income on housing expenses and no more than 36 percent on total debt -- that includes housing as well as things like student loans, car expenses, and credit card payments.What is considered a high interest rate for a mortgage?

According to the National Association of Federal Credit Unions, bank interest rates for a three-year unsecured loan range from 2.9% to 18.86%, with an average of 9.74%, which means anything over 10% is likely to be considered high.How long does it take to close with rocket mortgage?

Step 4: Prepare For Closing (About 1 Month) Get ready to close on your mortgage loan when you reach an agreement with your seller. Most lenders require 30 – 45 days to finalize the details of your loan and make sure your home meets your loan's minimum requirements.What type of mortgage is best?

Pros and cons at a glance| Mortgage type | Pros |

|---|---|

| Tracker mortgage | Rates are transparent Often the best value |

| Standard variable rate mortgage | None |

| Discount mortgage | Rates can be competitive Can be combined with a tracker mortgage |

| Offset mortgage | You can lower your interest repayments More flexible |

Is it better to be debt free or have a mortgage?

Pay off high-interest consumer debt: Credit card debt, personal loan debt, and car loan debt charge higher interest than mortgages, and you can't deduct the interest. You'll still be working toward becoming debt-free, but will save more in interest and get a better return on your money.How long should you be debt free before applying for a mortgage?

Try to avoid applying for credit in the three months before getting a mortgage - it could hinder your score and lead to rejection. Some recommend at least a six-month gap, to be absolutely safe.Why a mortgage is a bad idea?

There are two reasons why piling on mortgage debt to buy a home is actually a bad idea. It is lower interest rate debt than credit cards, but it can be dangerous if you're not budgeting correctly. So when mortgage debt is not a good idea is, one, essentially it's your single, largest monthly expense.What percent of take home pay should mortgage be?

28 percentHow do I get preapproved for a mortgage?

Steps to getting a mortgage preapproval- Get your free credit score. Know where you stand before reaching out to a lender.

- Check your credit history.

- Calculate your debt-to-income ratio.

- Gather income, financial account and personal information.

- Contact more than one lender.

How do I save up to buy a house?

How Much Should I Save for a Down Payment?- Determine how much you can afford each month.

- Use your monthly mortgage payment to arrive at a total mortgage amount.

- Aim for between 10% and 20% for your down payment.

- Start with a smaller number.

- Set up a Down Payment Fund.

- Throw extra money toward your Down Payment Fund.

Should I refinance my house Dave Ramsey?

Dave says no and that it's smart to refinance a house when you're looking for a lower interest rate. ANSWER: No, it's smart to refinance a house to have a lower interest rate, thereby paying off the home quicker. Some of you sitting there with a 6% rate, if you have a $300,000 mortgage, that saves you 2%.How can I pay my mortgage off quicker?

Pay Off Your House Quickly With These 7 Strategies- [Read: Credit, Mortgages and Your Ability to Buy a Home: It Doesn't Have to Be Scary.]

- Make biweekly payments.

- Budget for an extra payment each year.

- Send extra money for the principal each month.

- [See: 8 Financial Steps to Take After Paying Off a Debt.]

- Recast your mortgage.

- Refinance your mortgage.