What is the new FASB revenue recognition rule?

.

Just so, what is the new revenue recognition standard?

The new standard provides a comprehensive, industry-neutral revenue recognition model intended to increase financial statement comparability across companies and industries.

Subsequently, question is, what did ASC 606 Change? Accounting Standards Codification 606 (ASC 606) establishes new rules for US companies about booking revenues, in the process creating a common standard for Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS), which means similar changes are rolling out in most other

Also question is, what is the effective date of the new revenue recognition standard?

Effective Date for Private Companies As discussed above, for private companies, the new revenue standard is effective for annual reporting periods beginning after December 15, 2018, and interim reporting periods within annual reporting periods beginning after December 15, 2019.

What are the four criteria for revenue recognition?

The staff believes that revenue generally is realized or realizable and earned when all of the following criteria are met:

- Persuasive evidence of an arrangement exists,3

- Delivery has occurred or services have been rendered,4

- The seller's price to the buyer is fixed or determinable,5

- Collectibility is reasonably assured.

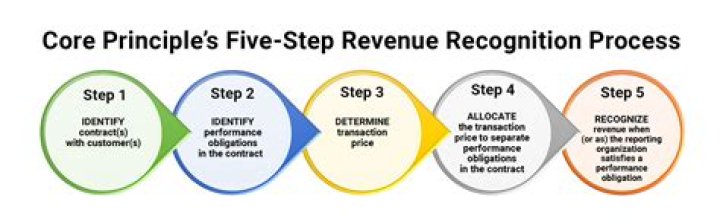

What are the five steps to revenue recognition?

Within the new standards there are five steps outlined for revenue recognition.- Step 1: Identify the contract with a customer.

- Step 2: Identify the performance obligations in the contract.

- Step 3: Determine the transaction price.

- Step 4: Allocate the prices to the performance obligations.

- Step 5: Recognize revenue.

When should revenue be recognized?

According to the principle, revenues are recognized when they are realized or realizable, and are earned (usually when goods are transferred or services rendered), no matter when cash is received. In cash accounting – in contrast – revenues are recognized when cash is received no matter when goods or services are sold.What is 606 revenue recognition?

ASC 606 is the new revenue recognition standard that affects all businesses that enter into contracts with customers to transfer goods or services – public, private and non-profit entities.When should a company recognize revenue under GAAP?

Note that the revenue recognition principle under GAAP stipulates that revenues are recognized when realized and earned, not necessarily when received. ("Realizable" means that goods and/or services have been received, but payment for the product/service is expected later).What is revenue recognition with example?

The revenue recognition principle states that one should only record revenue when it has been earned, not when the related cash is collected. For example, a snow plowing service completes the plowing of a company's parking lot for its standard fee of $100.What does GAAP say about revenue recognition?

Revenue recognition is a generally accepted accounting principle (GAAP) that identifies the specific conditions in which revenue is recognized and determines how to account for it. Typically, revenue is recognized when a critical event has occurred, and the dollar amount is easily measurable to the company.Who does ASC 606 apply to?

What is ASC 606? ASC 606/IFRS 15 accounting standards promise international alignment on how companies recognize revenue from contracts with customers. The guidelines are about the results of your end-to-end processes starting with contracts, through pricing, quotes, orders, and ending with revenue recognition.What is revenue recognition SAP?

SAP's revenue recognition functionality enables you to post the billing documents and recognize revenue at different points in time. In the regular process, SAP recognizes revenue as soon as the billing document is posted to accounting. Suppose you have to bill the customer first and recognize revenue later.How is the new revenue recognition standard different?

Hence the new revenue recognition standard. One of the key differences in this new revenue recognition standard is that it requires companies to disclose new information beyond data a company might have been required to release in the past.Why is the timing of revenue recognition important?

The most important reason to follow the revenue recognition standard is because it ensures that your books show what your profit and loss margin is like in real time. It's important to maintain credibility for your finances. Financial reporting helps keep your transactions aligned.What are prerequisites of revenue recognition?

According to the IFRS criteria, for revenue to be recognized, the following conditions must be satisfied:- Risks and rewards of ownership have been transferred from the seller to the buyer.

- The seller does not have control any longer over the goods sold.

- The collection of payment.

What is asc842?

Accounting Standards Codification Topic 842, also known as ASC 842 and as ASU 2016-02, is the new lease accounting standard published by the Financial Accounting Standards Board (FASB). he purpose of the new standard to close a major accounting loophole in ASC 840: off-balance sheet operating leases.What is the difference between ASC 605 and 606?

ASC 606 focuses on the transfer of control rather than the satisfaction of obligations prescribed by ASC 605. It's a principles-based framework that introduces more judgement into the revenue recognition process. Its core principles are focused on the nature of the promises in a contract.What is CECL model?

Current Expected Credit Losses (CECL) is a new credit loss accounting standard (model) that was issued by the Financial Accounting Standards Board (FASB) on June 16, 2016. The CECL standard focuses on estimation of expected losses over the life of the loans, while the current standard relies on incurred losses.What is deferred revenue in accounting?

Deferred revenue refers to payments received in advance for services which have not yet been performed or goods which have not yet been delivered. These revenues are classified on the company's balance sheet as a liability and not as an asset.How do you find contract revenue?

5 steps for revenue recognition- Identify the contract with a customer.

- Identify the performance obligations in the contract.

- Determine the transaction price.

- Allocate the transaction price to the performance obligations in the contract.

- Recognize revenue recognition when the performance obligation is fulfilled.