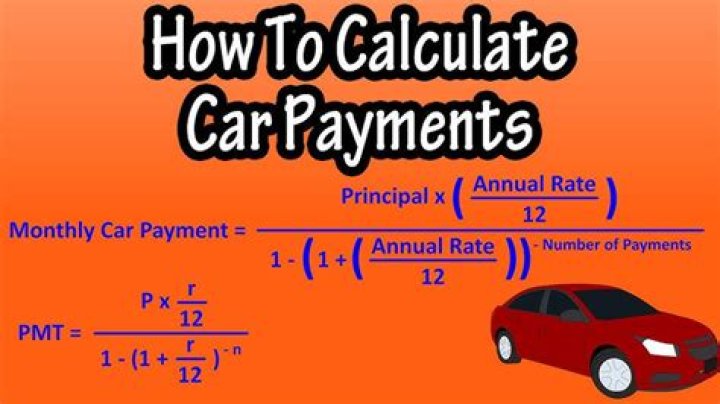

What is the formula for calculating a car payment?

- Use the formula A = P ∗ ( r ( 1 + r ) n ) / ( ( 1 + r ) n − 1 ) {displaystyle A=P*(r(1+r)^{n})/((1+r)^{n}-1)} .

- A = the monthly payment.

- P = the principal.

- r = the interest rate per month, which equals the annual interest rate divided by 12.

- n = the total number of months.

.

Moreover, how do you find out how much you owe on your car?

Contacting your lender is an easy way to find out how much money you owe on your car loan. You can usually find out by phone or by logging into your account on your lender's website to view the payoff amount.

how much total interest will I pay on a car loan? Use this loan interest calculator to see how much interest you can expect to pay your lender over the course of your loan. If you borrow $20,000 at 5.00% for 5 years, your monthly payment will be $377.42 and you will pay a total of $2,645.48 over the term of the loan.

Besides, what is the PMT formula?

The Excel PMT function is a financial function that returns the periodic payment for a loan. You can use the NPER function to figure out payments for a loan, given the loan amount, number of periods, and interest rate. rate - The interest rate for the loan. nper - The total number of payments for the loan.

How much should my car payment be?

According to this rule, when buying a car, you should put down at least 20 percent, you should finance the car for no more than 4 years, and you should keep your monthly car payment (including your principal, interest, insurance, and other expenses) at or below 10 percent of your gross (i.e. pre-tax) monthly income.

Related Question AnswersHow do you calculate total interest paid?

Calculate your total interest paid. This is done by subtracting your principal from the total value of your payments. To get your total value of payments, multiply your number of payments, "n," by the value of your monthly payment, "m." Then, subtract your principal, "P," from this number.How is installment calculated?

The equation to find the monthly payment for an installment loan is called the Equal Monthly Installment (EMI) formula. It is defined by the equation Monthly Payment = P (r(1+r)^n)/((1+r)^n-1). The other methods listed also use EMI to calculate the monthly payment. r: Interest rate.How is APR calculated on a car?

Lenders charge interest on a car loan each month. The amount of interest is obtained by multiplying the monthly interest rate by the loan balance. To calculate the APR, simply multiply the monthly rate by 12.How long is a car loan?

The most common term currently is for 72 months, with an 84-month loan not too far behind. It's been creeping up: 10 years ago, the most common new-car loan term was 60 months, followed closely by 72 months. Loans for used cars are about as long: The most common term for a used car in 2018 was 72 months.What is a car loan called?

A car loan (also known as an automobile loan, or auto loan) is a sum of money a consumer borrows in order to purchase a car. This type of loan is also known as financing. Car loans generally include a variety of fees and taxes, which are added to the total loan amount.How do you calculate monthly payments?

Multiply the amount you borrow by the annual interest rate. Then divide by the number of payments per year. Or, multiply the amount you borrow by the monthly interest rate, which is the annual interest rate divided by 12. Using the previous loan example, an annual interest rate of .Can you negotiate your car payoff?

In general, lenders aren't eager to negotiate your auto loan payoff balance. You signed an agreement to pay the borrowed funds back, and the car itself acts as security for it, so there's a built-in limit to the maximum loss the lender will be willing to take.Does paying off car loan early hurt your credit?

Installment loan accounts affect your credit score differently. And while paying off an installment loan early won't hurt your credit, keeping it open for the loan's full term and making all the payments on time is actually viewed positively by the scoring models and can help you credit score.Why is my payoff amount more than what I owe?

The payoff balance on a loan will always be higher than the statement balance. That's because the balance on your loan statement is what you owed as of the date of the statement. The lender will want to collect every penny in interest due to him right up to the day you pay off the loan.Can I get a loan to pay off my car?

Depending on your credit and repayment terms, you may only qualify for a personal loan that has a higher interest rate than your existing car loan. If this is the case, paying off the car loan may feel like progress, but you won't really be moving the needle on your debt. You're trading debt for debt.What happens when you pay off auto loan?

An auto loan is an installment account, or one with a level payment every month. Once your auto loan is repaid, you could lose points on your credit score, especially if you don't have other installment accounts. That's because a factor in your credit score is called “credit mix,” or types of credit accounts.How do I make a final car payment?

- Ask For the Payoff Amount. An outstanding loan balance will continue to accrue interest until it's paid in full.

- Keep Good Records. It's not a bad idea to hold onto proof that you paid off a loan, just in case someone tries to collect on it later.

- Stop Your Automatic Payment.

- Watch Your Credit.