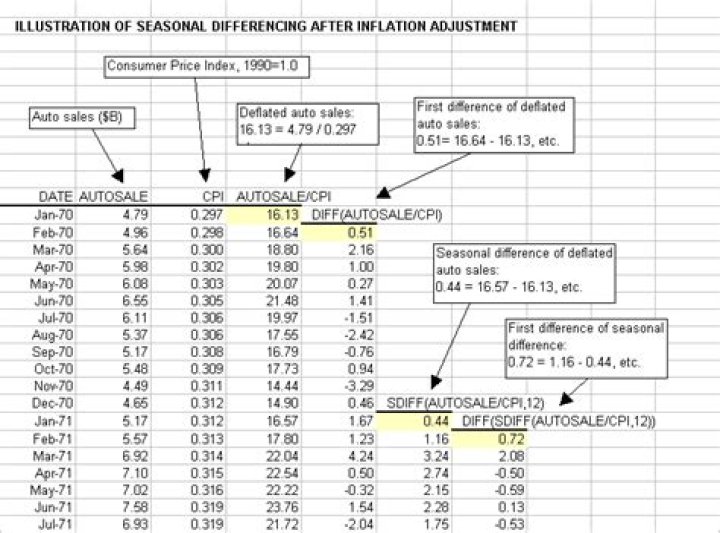

Seasonal differencing is a crude form of additive seasonal adjustment: the "index" which is subtracted from each value of the time series is simply the value that was observed in the same season one year earlier..

Hereof, does differencing remove seasonality?

Differencing can help stabilize the mean of the time series by removing changes in the level of a time series, and so eliminating (or reducing) trend and seasonality.

Also Know, is a seasonal time series stationary? A stable seasonal pattern is not stationary in the sense that the mean of the series will vary across seasons and, hence, depends on time; but it is stationary in the sense that we can expect the same mean for the same month in different years.

Thereof, how do I remove a seasonal cycle from data?

A simple way to correct for a seasonal component is to use differencing. If there is a seasonal component at the level of one week, then we can remove it on an observation today by subtracting the value from last week.

What does seasonality mean?

Seasonality is a characteristic of a time series in which the data experiences regular and predictable changes that recur every calendar year. Any predictable fluctuation or pattern that recurs or repeats over a one-year period is said to be seasonal.

Related Question Answers

How do you determine seasonality?

The following graphical techniques can be used to detect seasonality: - A run sequence plot will often show seasonality.

- A seasonal plot will show the data from each season overlapped.

- A seasonal subseries plot is a specialized technique for showing seasonality.

How do you know if a time series is stationary?

ADF (Augmented Dickey Fuller) Test Test for stationarity: If the test statistic is less than the critical value, we can reject the null hypothesis (aka the series is stationary). When the test statistic is greater than the critical value, we fail to reject the null hypothesis (which means the series is not stationary).How do you adjust Seasonality in Time Series?

In additive seasonal adjustment, each value of a time series is adjusted by adding or subtracting a quantity that represents the absolute amount by which the value in that season of the year tends to be below or above normal, as estimated from past data.What is stationary time series?

Statistical stationarity: A stationary time series is one whose statistical properties such as mean, variance, autocorrelation, etc. are all constant over time. Such statistics are useful as descriptors of future behavior only if the series is stationary.Why is stationarity important in time series?

Stationarity is an important concept in time series analysis. Stationarity means that the statistical properties of a time series (or rather the process generating it) do not change over time. Stationarity is important because many useful analytical tools and statistical tests and models rely on it.Why is second order differencing in time series needed?

For a discrete time-series, the second-order difference represents the curvature of the series at a given point in time. If the second-order difference is positive then the time-series is curving upward at that time, and if it is negative then the time series is curving downward at that time.What is seasonality in forecasting?

In statistics, the demand - or the sales - of a given product is said to exhibit seasonality when the underlying time-series undergoes a predictable cyclic variation depending on the time within the year. Seasonality is one of most frequently used statistical patterns to improve the accuracy of demand forecasts.What is the difference between trend and seasonally adjusted?

The process of estimating and removing seasonal patterns is known as seasonal adjustment. The trend is the underlying direction of the series - "what's normal". It smooths out most of the noise and short-term effects present in the seasonally adjusted.What is the difference between trend and seasonality?

These components are defined as follows: Level: The average value in the series. Trend: The increasing or decreasing value in the series. Seasonality: The repeating short-term cycle in the series.What does seasonally adjusted mean and how does this impact the numbers?

Seasonal adjustment is a statistical technique that attempts to measure and remove the influences of predictable seasonal patterns to reveal how employment and unemployment change from month to month. As a general rule, the monthly employment and unemployment numbers reported in the news are seasonally adjusted data.What is time series trend?

Web Service. OECD Statistics. Definition: The trend is the component of a time series that represents variations of low frequency in a time series, the high and medium frequency fluctuations having been filtered out.Should I use seasonally adjusted data?

Seasonally adjusted data are usually preferred in the formulation of economic policy and for economic research, because they eliminate the effects of changes that normally occur at the same time and in about the same magnitude every year.What is differencing in Arima?

D = In an ARIMA model we transform a time series into stationary one(series without trend or seasonality) using differencing. Differencing is a method of transforming a non-stationary time series into a stationary one. This is an important step in preparing data to be used in an ARIMA model.What is seasonal variation in statistics?

Seasonal Variation. It is a variable element in the time-series analysis of forecasting, and refers to the phenomenon where the production and plan of product change on a certain seasonal trend depending to the characteristics of the product.What are the four main components of a time series?

Time series consist of four components: (1) Seasonal variations that repeat over a specific period such as a day, week, month, season, etc., (2) Trend variations that move up or down in a reasonably predictable pattern, (3) Cyclical variations that correspond with business or economic 'boom-bust' cycles or follow theirWhat are the models of time series?

A linear time series model can be a polynomial ( idpoly ), state-space ( idss , or idgrey ) model. Some particular types of models are parametric autoregressive (AR), autoregressive and moving average (ARMA), and autoregressive models with integrated moving average (ARIMA).What are the types of time series analysis?

Methods for analysis Methods for time series analysis may be divided into two classes: frequency-domain methods and time-domain methods. The former include spectral analysis and wavelet analysis; the latter include auto-correlation and cross-correlation analysis.Why random walk is not stationary?

No, it is not. Random Walks are non stationary. But not all non stationary processes are random walks. A non stationary time series's mean and/or variance are not constant over time.What is trend stationary process?

Trend stationary: The mean trend is deterministic. Once the trend is estimated and removed from the data, the residual series is a stationary stochastic process. Difference stationary: The mean trend is stochastic. Differencing the series D times yields a stationary stochastic process.