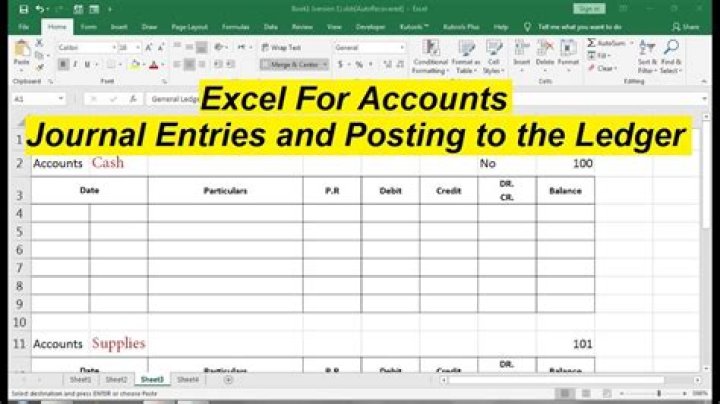

What is Ledger Posting in accounting?

.

Just so, what are ledgers in accounting?

An accounting ledger is an account or record used to store bookkeeping entries for balance-sheet and income-statement transactions. Accounting ledger journal entries can include accounts like cash, accounts receivable, investments, inventory, accounts payable, accrued expenses, and customer deposits.

Similarly, how do you prepare a ledger posting? The method of posting is as follows;

- firstly you can post the debit entry from journal to the ledger.

- to record the transaction date of the journal in the ledger account.

- The opposite account of debit is recorded in ledger account.

- the reference number of the journal records into the ledger account.

Subsequently, one may also ask, what is posting in accounting?

May 21, 2019. Posting in accounting is when the balances in subledgers and the general journal are shifted into the general ledger. Posting only transfers the total balance in a subledger into the general ledger, not the individual transactions in the subledger.

What is purpose of ledger?

The purpose of the ledger is to take the entries made in the journal and logs and tallies up all transactions that affect a specified account. The ledger does not show you the offsetting account.

Related Question AnswersWhat are the types of ledger?

Predominantly there are 3 different types of ledgers; Sales, Purchase and General ledger. A ledger is also known as the principal book of accounts and it forms a permanent record of all business transactions.What is Ledger example?

A ledger account contains a record of business transactions. It is a separate record within the general ledger that is assigned to a specific asset, liability, equity item, revenue type, or expense type. Examples of ledger accounts are: Cash.What is called ledger?

A ledger is the principal book or computer file for recording and totaling economic transactions measured in terms of a monetary unit of account by account type, with debits and credits in separate columns and a beginning monetary balance and ending monetary balance for each account.What is debit and credit?

A debit is an accounting entry that either increases an asset or expense account, or decreases a liability or equity account. It is positioned to the left in an accounting entry. A credit is an accounting entry that either increases a liability or equity account, or decreases an asset or expense account.What is the format of ledger?

The format of ledger account and posting process The information that has already been recorded in the journal is just transferred to the relevant ledger accounts in the general ledger. For the purpose of posting to general ledger, we can divide a journal entry into two parts – a debit part and a credit part.Why ledger is called the king of all books?

Ledger is called the king of all books of accounts because all entries from the books of original entry must be posted to the various accounts in the ledger. It should be noted that journal contains a chronological record while ledger contains a classified record of all transactions.What is contra entry?

Contra entry is a transaction which involves both cash and bank. Both debit aspect and credit aspect of a transaction get reflected in the cash book. For example: Cash received from debtors and deposited into bank. Cash withdrawn from bank for office use.What are four steps posting?

The five steps of posting from the journal to ledger include typing the account name and number, specifying the details of the journal entry, entering the debits and credits for the transaction, calculating the running debit and credit balances, and correcting any errors.What are the rules of posting?

Rules for posting of entries in the ledger The words like 'To' and 'By' are used while posting the entries in the ledger accounts. 'To' is used when accounts are posted in the debit side column of a particular account. 'By' is used when accounts are posted in the credit side column of a particular account.Why is posting important in accounting?

Posting is an important part of accounting since it helps to keep an updated record of all ledger balances & at the same time it can help a user to track how the ledger balances have changed over a period of time.What are the steps in making a journal entry?

The six steps of the accounting cycle:- Analyze and record transactions.

- Post transactions to the ledger.

- Prepare an unadjusted trial balance.

- Prepare adjusting entries at the end of the period.

- Prepare an adjusted trial balance.

- Prepare financial statements.

What is cash posting in accounting?

Cash posting is a process by which the payment gets received from customers, towards due payment and other accounts in the invoi. Page 1. Cash Posting. Cash posting is a process by which the payment gets received from customers, towards due payment and other accounts in the invoice system.When should Posting be done?

Posting is always from the journal to the ledger accounts. Postings can be made (1) at the time the transaction is journalized; (2) at the end of the day, week, or month; or (3) as each journal page is filled.What are the 8 steps in the accounting cycle?

Steps in the accounting cycle- #1 Transactions. Transactions: Financial transactions start the process.

- #2 Journal Entries. Journal Entries.

- #3 Posting to the General Ledger (GL)

- #4 Trial Balance.

- #5 Worksheet.

- #6 Adjusting Entries.

- #7 Financial Statements.

- #8 Closing.

What is a journal accounting?

In accounting and bookkeeping, a journal is a record of financial transactions in order by date. The definition was more appropriate when transactions were written in a journal prior to manually posting them to the accounts in the general ledger or subsidiary ledger.What is a proof of cash?

A proof of cash is essentially a roll forward of each line item in a bank reconciliation from one accounting period to the next, incorporating separate columns for cash receipts and cash disbursements.What is the difference between journal and ledger?

Key Differences Between Journal and Ledger When the transactions are entered in the journal, then they are posted into individual accounts known as Ledger. The Journal is a subsidiary book, whereas Ledger is a principal book. The Journal is known as the book of original entry, but Ledger is a book of second entry.How do you prepare a ledger journal?

How to Write and Prepare Ledger Account- Drawing the Form – Get pen and paper, start drawing the ledger account.

- Posting transactions from journal to respective ledger account.

- Folioing – Put the page number for a journal entry on the ledger account's folio column.

- Casting – Separating debit and credit amount.