Asset Retirement Obligation, Accretion Expense. Amount of accretion expense recognized in the income statement during the period that is associated with asset retirement obligations. Accretion expense measures and incorporates changes due to the passage of time into the carrying amount of the liability..

Keeping this in consideration, what does asset retirement obligation mean?

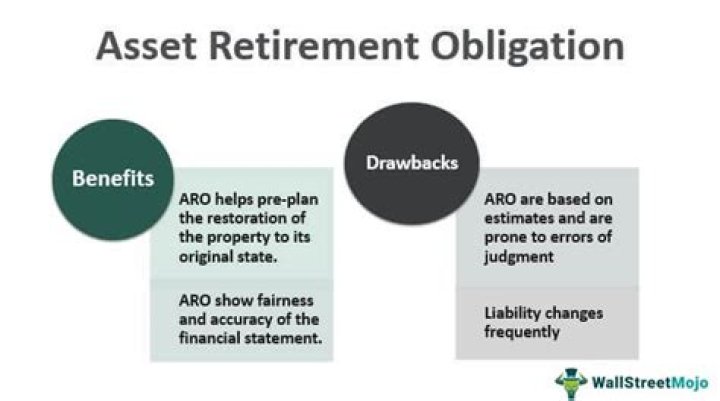

An Asset Retirement Obligation (ARO) is a legal obligation associated with the retirement of a tangible long-lived asset in which the timing or method of settlement may be conditional on a future event, the occurrence of which may not be within the control of the entity burdened by the obligation.

Subsequently, question is, how do you record an asset retirement obligation? When an asset retirement obligation is measured, an asset retirement cost is capitalized by increasing the carrying amount of the long-lived asset by the same amount as the liability. Since the asset retirement cost is included in the cost basis of the asset, it is subject to the regular depreciation process.

Likewise, people ask, how do you calculate asset retirement obligation?

Follow these steps in calculating the expected present value of an ARO:

- Estimate the timing and amount of the cash flows associated with the retirement activities.

- Determine the credit-adjusted risk-free rate.

- Recognize any period-to-period increase in the carrying amount of the ARO liability as accretion expense.

Is Asset retirement An obligations debt?

Asset retirement obligations are legal obligations associated with the retirement of long-lived assets that result from the acquisition, construction, development and/or the normal operation of such assets.

Related Question Answers

When must a company recognize an asset retirement obligation?

MEASUREMENT ISSUES Under Statement no. 143, an entity must recognize an asset retirement obligation at its fair value—the amount at which an informed willing party would agree to assume the obligation.What is retirement of fixed assets?

Fixed Asset Retirement and Disposal. Companies often remove fixed assets from service when those assets become obsolete because of physical (deterioration) or economic (technological innovation) factors. The remaining gross PP&E and accumulated depreciation of a sold asset are removed from the balance sheet.How do you retire an asset in SAP?

Asset Retirement with transaction code ABAVN - To retire an asset go to Navigation: SAP Easy Access -> SAP Menu -> Accounting -> Financial accounting -> Fixed Asset -> Posting -> Retirement -> Asset Retirement by Scrapping.

- Alternatively: Transaction code ABAVN.

What means Aro?

Noun. aro (plural aros) (slang, neologism) a person who is aromantic.What FAS 143?

FAS 143 means Financial Accounting Statement 143 promulgated by the Financial Accounting Standards Board. FAS 143 means Statement of Financial Accounting Standard 143 (and any statements replacing, modifying or superceding such statement) adopted by the Financial Accounting Standards Board.What is asset retirement SAP?

Asset retirement is the removal of an asset or part of an asset from the asset portfolio. An asset is sold, resulting in revenue being earned. The sale is posted with a customer. An asset is sold, resulting in revenue being earned. The sale is posted against a clearing account.What are decommissioning costs?

Decommissioning cost (also known as asset retirement obligation) is the cost incurred by companies in reversing the modifications made to landscape when a fixed asset is used up. An oil well offers a good example of asset that carries significant decommissioning cost.What is credit adjusted risk free rate?

Credit-adjusting the risk-free rate means adding to the Treasury rates some amount of additional interest-rate basis points to reflect the fact that companies might default on their debt obligations.What is accretion accounting?

In accounting, an accretion expense is a periodic expense recognized when updating the present value of a balance sheet liability, which has arisen from a company's obligation to perform a duty in the future, and is being measured by using a discounted cash flows ("DCF") approach.What is asset remediation?

Asset Remediation Corporation (ARC) ARC's primary product is three-phased (Assessment, Valuation and Disposition) in order to monetize toxic assets currently residing on the balance sheets of financial institutions, insurance companies, hedge funds and other corporations.How do you account for decommissioning costs?

The amount recognized for decommissioning costs is the present value of the expected future decommissioning costs. The present value is calculated as follows: Future cost x discount factor (2025), which is $80 million × 0.677 = $54.160 million.Are decommissioning costs Capitalised?

These costs should be capitalised at the date on which the entity becomes obligated to incur them. There may be significant changes in the initial (and subsequent) estimates of decommissioning costs of an asset, particularly where asset lives are long.What is accretion in oil and gas?

Accretion expense is the ongoing, scheduled recognition of an expense related to a long-term liability. The amount charged to expense represents the change in the remaining discounted cash flows of the liability.Is accretion expense tax deductible?

The accretion expense associated with the ARO is not deductible for tax because the all events test of IRC § has not been met. This liability is discounted and accretion expense (operating expense) is recognized over time.