What can FHA loans be used for?

.

People also ask, is an FHA loan bad?

FHA-backed loans usually have more lenient requirements than conventional loans—lower credit scores are required and your down payment can be as low as 3.5 percent. The FHA loan is reserved for first time home buyers and only available through FHA lenders.

Also Know, what can you buy with an FHA loan? Hazards aside, you can buy several types of homes with an FHA loan. These include regular detached homes, row houses, condos, semi-detached, and multiplex / multifamily units.

Similarly, it is asked, how does an FHA loan work?

An FHA loan is a mortgage that's insured by the Federal Housing Administration (FHA). However, borrowers must pay mortgage insurance premiums, which protects the lender if a borrower defaults. Borrowers can qualify for an FHA loan with a down payment as little as 3.5% for a credit score of 580 or higher.

When can you use an FHA loan?

To recap the numbers: FHA loans are available to individuals with credit scores as low as 500. If your credit score is between 500 and 579, you can get an FHA loan with a down payment of 10%. If your credit score is 580 or higher, you can get an FHA loan with as little as 3.5% down.

Related Question AnswersWhy do sellers hate FHA loans?

The other major reason sellers don't like FHA loans is that the guidelines require appraisers to look for certain defects that could pose habitability concerns or health, safety, or security risks. If any defects are found, the seller must repair them prior to the sale.What are the disadvantages of FHA loans?

Here are some of the disadvantages of using an FHA home loan to buy a house.- Higher Interest Rates. You will probably be assigned a higher interest rate than if you had used a conventional mortgage loan.

- Mortgage Insurance Premiums - Two of Them.

- Condo Restrictions.

- The Multiple-Offer Disadvantage.

Is conventional loans better than FHA?

1) Credit score: Buyers with low-to-average credit scores may be better suited for an FHA loan. FHA mortgage rates are lower than conventional ones for applicants with “dinged” credit, and FHA loans allow credit scores down to 580. 2) Down payment: You get a lower down payment option with conventional, at just 3% down.What is the income limit for FHA loan?

Short answer: The general rule for FHA loans is 43% debt-to-income ratio. This means your combined debts should use no more than 43% of your gross monthly income — after taking on the loan. But there are exceptions.How hard is it to get a FHA loan?

You can get approved for an FHA mortgage loan with a 500-579 credit score with 10% down. However, it is very difficult to process a loan application with a credit score in this range. If you have at least a 580 credit score, it is easier to qualify for an FHA mortgage.What is the current interest rate on FHA loans?

FHA loan interest rates| Term | Rate | APR |

|---|---|---|

| 30-year fixed - FHA | 4.250% | 5.315% |

| 15-year fixed - FHA | 3.875% | 4.948% |

Can you get rid of PMI on FHA loan?

By law, lenders must cancel conventional PMI when you reach 78% loan-to-value. Many home buyers opt for a conventional loan, because PMI drops, while FHA MIP typically does not. Keep in mind that most lenders base the 78% LTV on their last appraised value. You can also cancel conventional PMI with a refinance.What are the requirements for a FHA loan?

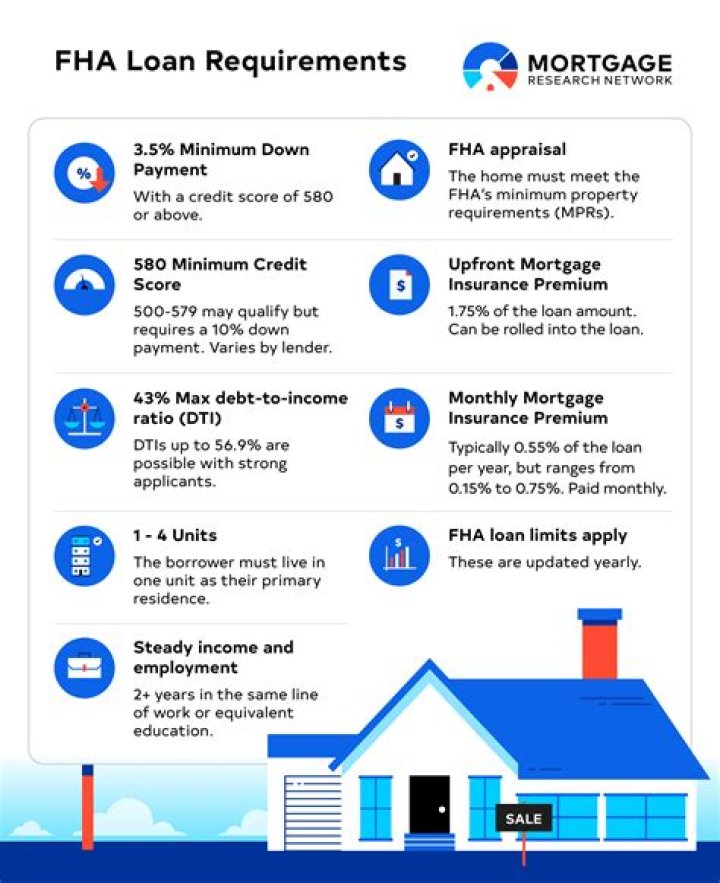

FHA Loan Requirements- FICO® score at least 580 = 3.5% down payment.

- FICO® score between 500 and 579 = 10% down payment.

- MIP (Mortgage Insurance Premium ) is required.

- Debt-to-Income Ratio < 43%.

- The home must be the borrower's primary residence.

- Borrower must have steady income and proof of employment.