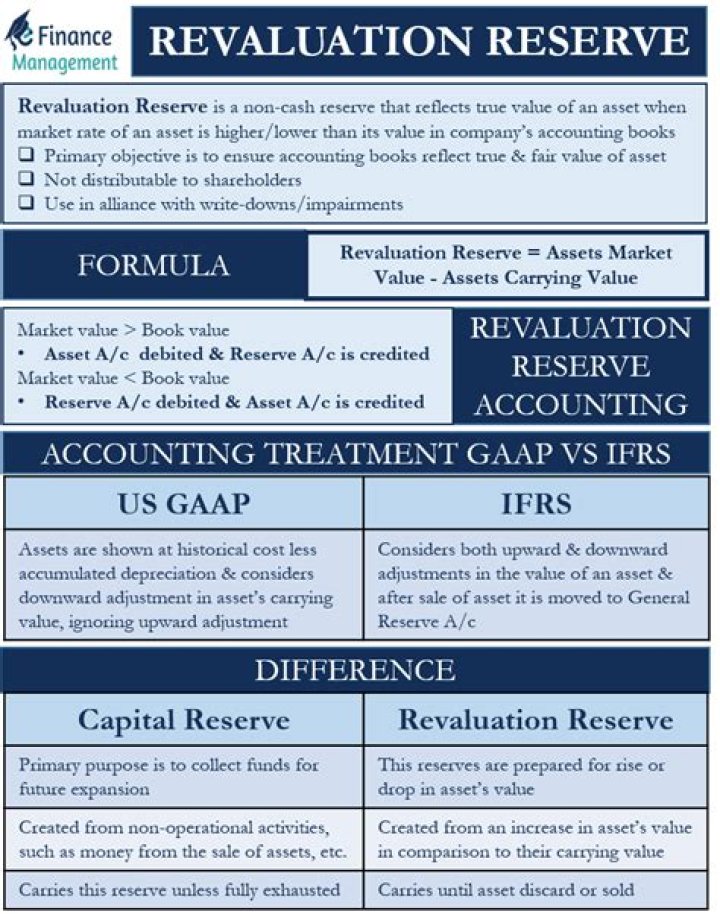

ASSET REVALUATION RESERVE Definition. ASSET REVALUATION RESERVE is an accounting concept and represents a reassessment of the value of a capital asset as at a particular date. The reserve is considered a category of the equity of the entity..

Simply so, what is a revaluation reserve on the balance sheet?

Definition: Revaluation Reserve If the value of the asset increases over the current amount accounted for in the balance sheet (that is, if the current market value of the asset exceeds the amount accounted for in the balance sheet), we go for its revaluation.

Beside above, what type of account is asset revaluation reserve? Revaluation reserve is an accounting term used when a company creates a line item on its balance sheet for the purpose of maintaining a reserve account tied to certain assets. This line item can be used when a revaluation assessment finds that the carrying value of the asset has changed.

Subsequently, one may also ask, is revaluation surplus an asset?

Revaluation surplus. A revaluation surplus is an equity account in which is stored any upward changes in the value of capital assets. If a revalued asset is subsequently dispositioned out of a business, any remaining revaluation surplus is credited to the retained earnings account of the entity.

What is the journal entry for revaluation of assets?

A revaluation that increases or decreases an asset 's value can be accounted for with a journal entry that will debit or credit the asset account. An increase in the asset's value should not be reported on the income statement; instead an equity account is credited and called a “Revaluation Surplus”.

Related Question Answers

What does revaluation reserve mean in accounting?

Revaluation reserve is an accounting term used when a company creates a line item on its balance sheet for the purpose of maintaining a reserve account tied to certain assets. This line item can be used when a revaluation assessment finds that the carrying value of the asset has changed.How do you record an asset revaluation?

Key Points - A revaluation that increases or decreases an asset 's value can be accounted for with a journal entry that will debit or credit the asset account.

- An increase in the asset's value should not be reported on the income statement; instead an equity account is credited and called a “Revaluation Surplus”.

How is revaluation reserve treated?

Revaluation Reserve is treated as a Capital Reserve. The increase in depreciation arising out of revaluation of fixed assets is debited to revaluation reserve and the normal depreciation to Profit and Loss account. Selection of the most suitable method of revaluation is extremely important.What is revaluation reserve used for?

Revaluation reserve is an accounting term used when a company creates a line item on its balance sheet for the purpose of maintaining a reserve account tied to certain assets. This line item can be used when a revaluation assessment finds that the carrying value of the asset has changed.How do you account for revaluation?

Key Points - A revaluation that increases or decreases an asset 's value can be accounted for with a journal entry that will debit or credit the asset account.

- An increase in the asset's value should not be reported on the income statement; instead an equity account is credited and called a “Revaluation Surplus”.

Where does revaluation reserve go in balance sheet?

Asset Revaluation Reserves, which arise when a company has to adjust the value of an asset that is carried in the asset section of its balance sheet and needs an offsetting transaction.What are the 3 types of reserves?

There are different types of reserves used in financial accounting like capital reserves, revenue reserves, statutory reserves, realized reserves, unrealized reserves.Is revaluation reserve part of retained earnings?

When an asset is disposed of that has previously been revalued, a profit or loss on disposal is to be calculated (as above). Any remaining surplus on the revaluation reserve is now considered to be a 'realised' gain and therefore should be transferred to retained earnings as: Dr Revaluation reserve. Cr RetainedWhat is the double entry for revaluation?

Revaluation gains Double entry: Dr Non-current asset cost (difference between valuation and original cost/valuation) Dr Accumulated depreciation (with any historical cost accumulated depreciation) Cr Revaluation reserve (gain on revaluation)What is the difference between revaluation reserve and revaluation surplus?

The change in value is credited to the revaluation surplus (reserve) account. A downward revaluation is considered impairment. Revaluation Surplus (Reserve) - The increase in value of fixed assets due to the revaluation of the fixed assets is credited to revaluation surplus (reserve).Can you have a negative revaluation reserve?

In cases of negative revaluation – i.e. when an asset's book value decreases due to impairment – the loss should be written off against any revaluation surplus. If the loss exceeds the surplus, or if there is no surplus, the difference should be reported as an impairment loss.How do you account for revaluation surplus?

A revaluation that increases or decreases an asset 's value can be accounted for with a journal entry that will debit or credit the asset account. An increase in the asset's value should not be reported on the income statement; instead an equity account is credited and called a “Revaluation Surplus”.Where does revaluation loss go?

Revaluation losses are recognised in the income statement. The only exception to this rule is where a revaluation surplus exists relating to a previous revaluation of that asset. To that extent, a revaluation loss can be recognised in equity.How do you depreciate a revalued asset?

Under cost model depreciation is calculated on the basis of cost less residual value over the useful life of asset. Under revaluation model depreciation is calculated on the basis of revalued amount less residual value over the remaining useful life.Is revaluation reserve a capital reserve?

The 'Revaluation Reserve' is treated as a Capital Reserve as it cannot be distributed as dividends. However, if the asset has been sold at a profit, such profit is credited to Profit and Loss Account and the revaluation reserve balance is transferred to General Reserve Account.What is revaluation method?

Definition and meaning - InvestorGuide.com. Glossary > Accounting > revaluation method. revaluation method. a method of calculating the depreciation of assets, by which the asset is depreciated by the difference in its value at the end of the year over its value at the beginning of the year.Is revaluation reserve taxable?

When an NCA is revalued to its current value within the financial statements, the revaluation surplus is recorded in equity (in a revaluation reserve) and reported as other comprehensive income. Tax will become payable on the surplus when the asset is sold and so the temporary difference is taxable.Is revaluation reserve a free reserve?

Free reserves means reserves which, as per the latest audited balance sheet of a company, are available for distribution as dividend except the following: Any amount representing unrealised gains, notional gains or revaluation of assets, whether shown as a reserve or otherwise, or b.What is revaluation of assets and liabilities?

Revaluation of assets and liabilities. When a partner is admitted into the partnership, the assets and liabilities are revalued as the current value may differ from the book value. Determination of current values of assets and liabilities is called revaluation of assets and liabilities.