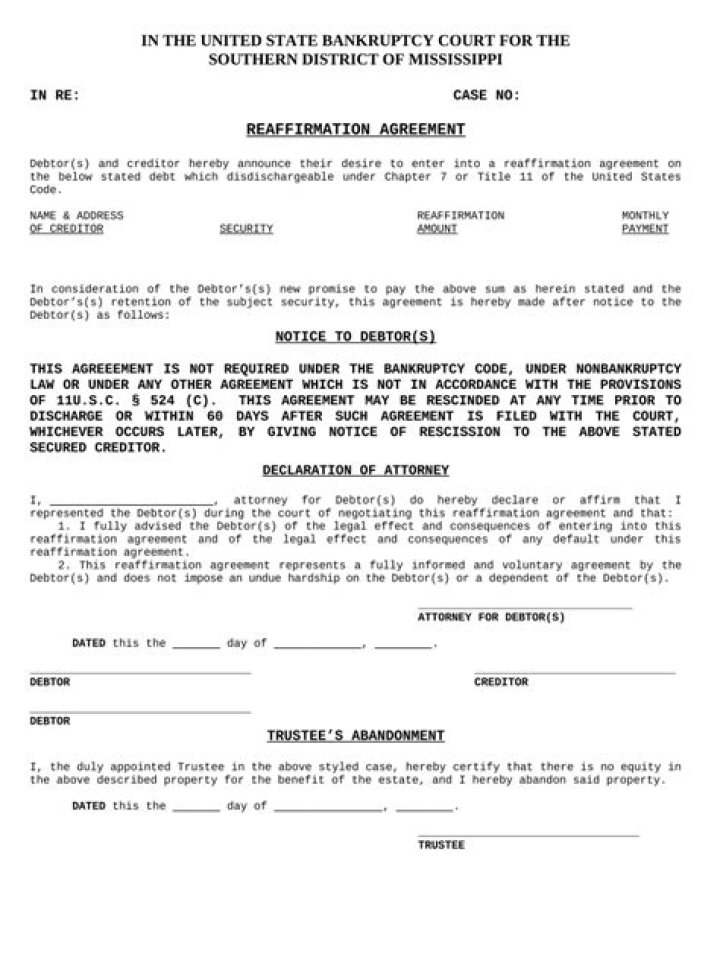

Reaffirmation agreements, although required by the bankruptcy laws for every secured debt that the debtor will continue to pay, are often not necessary in practice. The creditor, however, wants money, not collateral, so the creditor prefers to continue to receive payments and interest rather than take the collateral..

In this way, is a reaffirmation agreement required?

Reaffirmation agreements are strictly voluntary. A debtor is not required to reaffirm any of his or her debts. If a debtor signs a reaffirmation agreement, the debtor agrees to pay a debt that otherwise might be discharged in his or her bankruptcy case.

Similarly, what is the purpose of a reaffirmation agreement? From Wikipedia, the free encyclopedia. A reaffirmation agreement in United States bankruptcy law refers to an agreement made between a creditor and the debtor that waives discharge of a debt that would otherwise be discharged in the pending bankruptcy proceeding.

Simply so, what happens if you don't sign a reaffirmation agreement?

Failure to Reaffirm a Loan If no signed reaffirmation is filed, then the bankruptcy rules prevail -- and the creditor has the right to repossess collateral, as long as it's non-exempt property. If the court discharges the debt, then you can keep your property and no longer need to make payments.

What is a valid reaffirmation agreement?

A reaffirmation agreement is an agreement by which a bankruptcy debtor becomes legally obligated to pay all or a portion of an otherwise dischargeable debt. A debtor can voluntarily repay any debt instead of signing a reaffirmation agreement, but there may be valid reasons for wanting to reaffirm a particular debt.

Related Question Answers

How does reaffirmation agreement work?

Reaffirmation is the process wherein you agree to remain responsible for a debt so that you can keep the property securing the debt (collateral). You and the lender enter into a new contract—usually on the same terms—and submit it to the bankruptcy court.What happens if I don't reaffirm my car loan?

The bankruptcy cancels your legal liability to pay on the car. Failing to complete the reaffirmation will allow the lender to repossess the vehicle after your bankruptcy is completed. If that does happen, you will not be liable for the remaining balance because you did not reaffirm the loan.Can you negotiate a reaffirmation agreement?

When making an offer on a reaffirmation agreement, ask the lender to reduce the loan balance and the interest rate. Remember, this is a negotiation. You can expect the lender to come back with a counter offer. So, make your starting offer lower than the amount you are really willing to pay.What happens if I don't reaffirm my mortgage?

A reaffirmation agreement with a mortgage lender means you agree to keep up payments, and that the court will not discharge the loan. Since the lender will still have a lien on the property, however, you risk foreclosure if you cease payments after the bankruptcy, with or without a reaffirmation agreement.Can I cancel a reaffirmation agreement?

Yes. You can cancel (or “rescind”) your reaffirmation agreement, even if a judge has already approved it. NOTE: WE STRONGLY RECOMMEND THAT YOU SPEAK WITH AN ATTORNEY TO ADVISE YOU ABOUT THE CONSEQUENCES OF CANCELLING A REAFFIRMATION AGREEMENT IN YOUR CASE.How do I get a reaffirmation agreement?

To reaffirm a debt, you and the creditor agree to the terms of the new debt in a written reaffirmation agreement, which is filed with the court. You must file two court forms: Form 27 (the reaffirmation cover sheet) and Form 240A (the reaffirmation agreement itself.)Can I sell my house if I did not reaffirm?

Yes, you can sell the home. The effect of no reaffirmation is that you do not have a personal obligation to pay the mortgage. You still are the titled owner and the mortgage is still a lien on the property so it must be paid in order to sell the property.Can I file a reaffirmation agreement after discharge?

Reaffirmation agreements must be signed before the debtor gets his discharge in the bankruptcy. The debtor must then file a motion to reopen the bankruptcy case, then file a second motion to vacate the discharge, then file the reaffirmation agreement with the court. Most courts will not allow debtors to do this.Does reaffirming help credit?

Reaffirming Helps to Rebuild Your Credit This means that the timely payments you make will not help you in establishing a good credit history after bankruptcy. If you reaffirm the loan, your lender will continue reporting your payments which will help you in establishing good credit.What happens after reaffirmation agreement?

Effect of a reaffirmation agreement. When you reaffirm a debt, you agree to be responsible for the debt as if you had not filed bankruptcy. Once you receive your discharge, you're bound by the agreement unless you rescind it within 60 days of the signing (see below).How long must you wait between bankruptcies?

You must wait at least 6 years from the date of filing your previous Chapter 13 bankruptcy, to file for Chapter 7 bankruptcy and receive a discharge (unless the exception applies).Can I refinance if I did not reaffirm my mortgage?

If you didn't reaffirm your debt, you might still be able to refinance later, as long as you still legally own the home. However, if you didn't reaffirm the debt, you can't refinance the loan with the same lender because of bankruptcy laws. So you'll have to find a new lender to refinance the loan.What happens if I miss my reaffirmation hearing?

2009), make clear that if the debtor fails either to reaffirm the debt or redeem the item within 45 days after the first meeting of creditors, then the stay terminates and the creditor can repossess, even if the debtor is current on the payments.Can I trade in my car after reaffirmation?

You can trade it in as long as your loan covers the payoff amount of your current car. You have 60 days to rescind a reaffirmation agreement.Is Chapter 7 or 11 worse?

The main difference between Chapter 7 and Chapter 11 bankruptcy is that under a Chapter 7 bankruptcy filing, the debtor's assets are sold off to pay the lenders (creditors) whereas in Chapter 11, the debtor negotiates with creditors to alter the terms of the loan without having to liquidate (sell off) assets.How can I reaffirm my mortgage?

A reaffirmation must be filed with the Court before discharge. Once discharge has been entered, it is too late to reaffirm a debt. Theoretically you would have to reopen the bankruptcy, set aside your discharge, and then reaffirm the debt, then get your discharge reentered, and close the case.What happens at a 341 meeting?

At the meeting of creditors—also called the 341 hearing—the debtor meets with the trustee appointed to oversee the case. The trustee will check identification and ask a series of questions about the bankruptcy paperwork. Creditors can attend and ask about financial matters as well, although few appear.How long do you have to reaffirm a mortgage?

Be sure to evaluate all of your options carefully and understand the consequences fully before deciding to reaffirm any debt. However, you must decide quickly because reaffirmation agreements must be filed with the court no later than 60 days after your 341(a) meeting of creditors.What is reaffirmation of faith?

reaffirm. To reaffirm is to make a renewed commitment to something, usually verbally. If you affirm something, you are saying "I believe in this!" So reaffirming repeats your belief, making it clear that you still feel that way.