For many home buyers, paying down and closing a credit line may improve the borrower's total debt service ratio, a key metric that lenders use when deciding whether to approve a loan. By paying off the line of credit, their debt-to-income ratio drops and this increases the amount they can borrow on a mortgage..

Besides, can a line of credit hurt your credit score?

When you apply for the line of credit, the lender may perform a hard inquiry on your credit reports. This could temporarily lower your credit scores by a few points. If you borrow a high percentage of the line, that could increase your utilization rate, which may hurt your credit scores.

Subsequently, question is, will my debt affect my mortgage application? If you have no borrowing to take into account, your credit score is likely to be too low for many lenders to approve you for a mortgage. If you're paying interest on credit card debt, this will negatively affect your disposable income and could therefore harm your application.

Also question is, does credit card limit affect mortgage approval?

A high credit limit could help or hurt your mortgage application. A credit utilization ratio measures how much of your available credit you're using. Some lenders however may view high credit limits as potential additional debt you could run up at any time, making it harder for you to get a mortgage.

What credit score is needed for a line of credit?

The personal line of credit is unsecured, so to get one, you probably will need a credit score at or above 700 and have a good history of repaying debts in a timely fashion.

Related Question Answers

What hurts your credit score the most?

- Missing a card or loan payment. Payment history accounts for 35 percent of your FICO score.

- Maxing out a credit card. Credit utilization accounts for 30 percent of your FICO score.

- Hard inquiries.

- Applying for too many credit cards.

- Collections and charge-offs.

- Bankruptcy.

- Foreclosure.

- Deed in lieu.

How long does a line of credit last?

How Do Lines of Credit Work? Your line of credit will have a "draw period" and a "repayment period." You borrow from the pool of money during the draw period. This might be for 10 years or so. You'll repay the principal and interest on the loan during the repayment period.Can you withdraw money from a line of credit?

A line of credit, or LOC, is a type of bank loan where you can withdraw up to an agreed upon amount. A line of credit only requires you to pay interest and fees on the portion of funds you borrow. If your line of credit is for $10,000 and you don't withdraw any money, you won't have to pay any interest.Should I accept a line of credit?

If you have more than one source of credit, it is also better to spread the balance over each card or line of credit. But if you accept a pre-approved increase to $10,000, and you continue to spend $2,000 each month, you are only using 20% of your available credit, which is within the recommended ratio range.What are the 3 C's of credit?

A credit score is dynamic and can change positively or negatively depending upon how much debt you accrue and how you manage your bills. The factors that determine your credit score are called The Three C's of Credit — Character, Capital and Capacity.Should I use my line of credit to pay credit card?

This is the main reason it's great to use a line of credit to pay off credit card debt. Typically, lines of credit have much lower interest rates than credit cards, which will reduce the overall carrying cost of your debt. For example, a $5,000 balance on a credit card at 20% will cost you $1,000 per year in interest.Is it bad to get a line of credit?

a personal line of credit is a bad idea. A person who has debt issues is unlikely to qualify for a personal signature loan or line of credit but even if they qualify, they are going deeper into debt. This is much like taking out payday loans because there are no other options.Is it better to have a line of credit or credit card?

Generally speaking, a credit card is better for purchases. A personal line of credit is better for cash advance. Banks don't advertise personal lines of credit as much as they do for credit cards.Can I buy a house with maxed out credit cards?

You can buy a house while in debt. It all depends on what portion of your monthly gross income goes towards paying the minimum amounts due on recurring debts like credit card bills, student loans, car loans, etc. Your debt-to-income ratio matters a lot to lenders. $1,916 goes towards debt.Should I pay off credit card debt before applying for a mortgage?

When you apply for a mortgage, you usually don't need to pay off all of your credit cards. However, it's normally better to have less debt than more debt.How much debt can you have and still qualify for a mortgage?

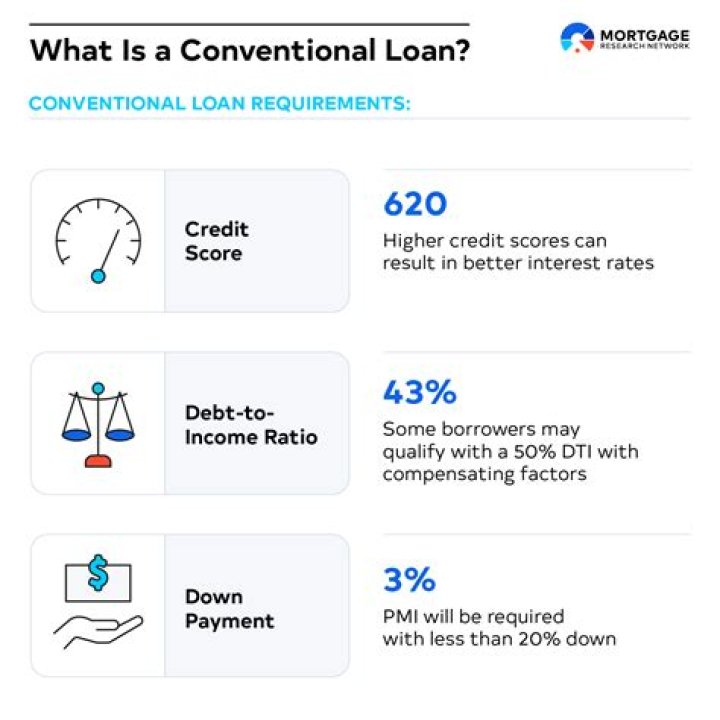

But these days, most lenders set the bar somewhere around 43% to 50%. That means that if your combined monthly debts (including the mortgage payment) exceed 50% of your income, you might have trouble qualifying for a mortgage loan. But those aren't hard and fast rules.Can you have too much available credit?

From the standpoint of increasing your credit scores, you can't have too much available credit. Having a very low credit utilization ratio, such as one that's under 10%, can only help your credit scores. However, there are a few other potential problems with having a large amount of available credit.Can you add credit card debt into new mortgage?

Turning credit card debt into a mortgage turns this money into a secured debt. That means you are tying an asset to the debt. Depending on how long your new repayment plan lasts, you may end up spending more in total interest costs over the course of the loan.Do lenders pull credit day of closing?

Here's the short answer: Most lenders who offer FHA loans will check your credit score at least twice. They do an initial pull shortly after you apply for financing, and they often do a second pull just before the scheduled closing day. Any major changes could potentially derail your loan.Should I increase my credit limit before buying a house?

Increase credit limit on an existing account (even if you don't plan to use it) Under ordinary circumstances, increasing your credit limit might improve your credit-utilization ratio (and thus your FICO score). However, this isn't the case when it's time to apply for a mortgage.Can I get a mortgage if I have credit card debt?

Well, fear not – a loan or credit card debt won't necessarily stop you from getting a mortgage. But the amount of debt you have will certainly influence how much you can borrow.Can you get a mortgage with a lot of credit card debt?

There's no need to fret, because you can get a mortgage if you have credit card debt.Many borrowers apply for a mortgage while carrying credit card debt. In fact, 175 million Americans actively use credit cards, and almost half (44%) don't pay their balance in full each month.How far back do Mortgage Lenders look at credit history?

There are many factors that lenders consider when looking at your credit history, and each one is different. The typical timeframe is the last six years, but there are many different factors that lenders look at when reviewing your mortgage application.What is a good credit score for a mortgage?

model for credit scores, which grades consumers on a 300- to 850-point range, with a higher score indicating less risk to the lender. A score of 800 or higher is considered exceptional; 740 to 799 is very good; 670 to 739 is good; 580 to 669 is fair; and 579 or lower is poor.