Can you amortize trademarks? | ContextResponse.com

.

Regarding this, how do you amortize trademark costs?

To determine how much to amortize the trademark by every year, take the original value of the copyright and divide by the remaining years of the trademark's term. The result is the annual amortization expense. To amortize the trademark, decrease the trademark's asset value by the annual amortization expense.

Similarly, do you amortize goodwill? Under US GAAP and IFRS, goodwill is never amortized, because it is considered to have an indefinite useful life. Instead, management is responsible for valuing goodwill every year and to determine if an impairment is required.

Also know, how intangible assets are amortized?

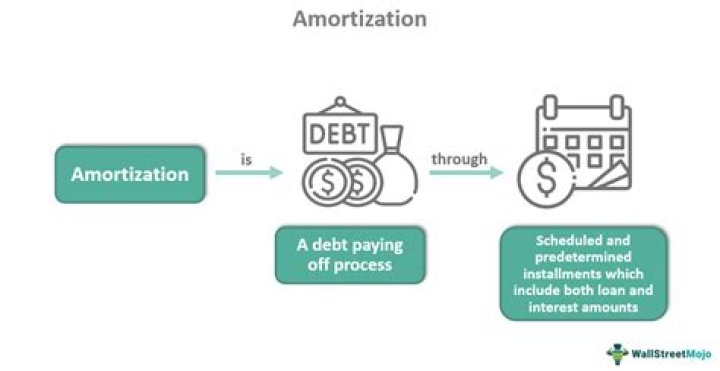

Amortization of intangibles is the process of expensing the cost of an intangible asset over the projected life of the asset. Intangible assets, such as patents and trademarks, are amortized into an expense account. Tangible assets are posted to expenses through depreciation.

Do you amortize intellectual property?

Accounting for Intellectual Property in Financial Statements These must be amortized over the useful life of the asset. When intellectual property is purchased from another business, it is recorded on the balance sheet at cost and amortized over the remaining useful life of the asset.

Related Question AnswersIs a trademark tax deductible?

Are trademark fees tax deductible? As a general, rule all of the costs of running a business are subtracted from revenue to get to profit (or income). As such trademark fees are clearly a cost and are deductible (and they are obviously revenue for the entity that is licensing the trade mark).What is the legal life of a trademark?

A trademark has a lifespan of 10 years from the date of registration. You must renew a trademark every 10 years in order to keep the registration active. Failure to file renewal within the stipulated deadline cancels the trademark and diminishes its value.Is trademark an asset or expense?

A trademark should be reported on the balance sheet as an intangible asset. However, the cost principle prevents the reported amount from being more than the cost of acquiring and defending the trademark.Is trademark an intangible asset?

An intangible asset is an asset that is not physical in nature. Goodwill, brand recognition and intellectual property, such as patents, trademarks, and copyrights, are all intangible assets.Is Amortization an operating expense?

Amortization appears on the Income Statement as an expense, like depreciation expense, usually under Operating Expenses, (or "Selling, General and Administrative Expenses). Amortization is a non-cash expense, but it nevertheless impacts the Statement of changes in financial position SCFP (Cash flow statement).How do you account for a trademark?

The following entries should be posted in accounting records:- The documents for the trademark registration were filed and respective fees were charged: Account Titles. Debit. Credit.

- The legal fees were paid: Account Titles. Debit. Credit.

- The company successfully registered the new trademark:

Is Amortization an asset?

Amortization refers to capitalizing the value of an intangible asset over time. It's similar to depreciation, but that term is meant to refer more to a tangible asset (a piece of equipment or office furniture that a company might purchase).Why do we amortize?

Amortization is a simple way to evenly spread out costs over a period of time. Typically, we amortize items such as loans, rent/mortgages, annual subscriptions and intangible assets. In order to spread the total cost according to the agreement evenly over the life of the terms, we amortize.Is intangible asset depreciable?

Intangible assets are non-physical assets on a company's balance sheet. If an intangible asset has a finite useful life, the company is required to amortize it, a process very similar to how physical assets are depreciated over time.How long do you amortize intangible assets?

15 yearsIs goodwill an intangible asset?

Goodwill is recorded as an intangible asset on the acquiring company's balance sheet under the long-term assets account. Goodwill is considered an intangible (or non-current) asset because it is not a physical asset like buildings or equipment.Which intangible asset is not amortized?

GoodwillIs Goodwill a debit or credit?

Goodwill is created when the purchase price of an acquired company exceeds the value of that company's net assets. Record Goodwill on the balance sheet of the company that acquired the other. Credit the acquired asset account, credit Goodwill, and debit the cash account.What is goodwill example?

Goodwill is created when one company acquires another for a price higher than the fair market value of its assets; for example, if Company A buys Company B for more than the fair value of Company B's assets and debts, the amount left over is listed on Company A's balance sheet as goodwill.Is there goodwill in a stock acquisition?

In a stock purchase, all of the assets and liabilities of the seller are sold upon transfer of the seller's stock to the acquirer. The acquirer does not receive a stepped-up tax basis in the acquired net assets but, rather, a carryover basis. Any goodwill created in a stock acquisition is not tax-deductible.What happens to existing goodwill in an acquisition?

In the event that an asset acquired during an M&A transaction does not qualify as an intangible based on these definitions, the asset will then be included as goodwill. The excess of the purchase price of the target business over the fair market value of the net assets is known as acquired goodwill.What are the types of goodwill?

There are two distinct types of goodwill: purchased, and inherent.- Purchased Goodwill. Purchased goodwill comes around when a business concern is purchased for an amount above the fair value of the separable acquired net assets.

- Inherent Goodwill.