Can mortgage points be deducted on taxes?

.

Likewise, are Mortgage Points deductible in 2019?

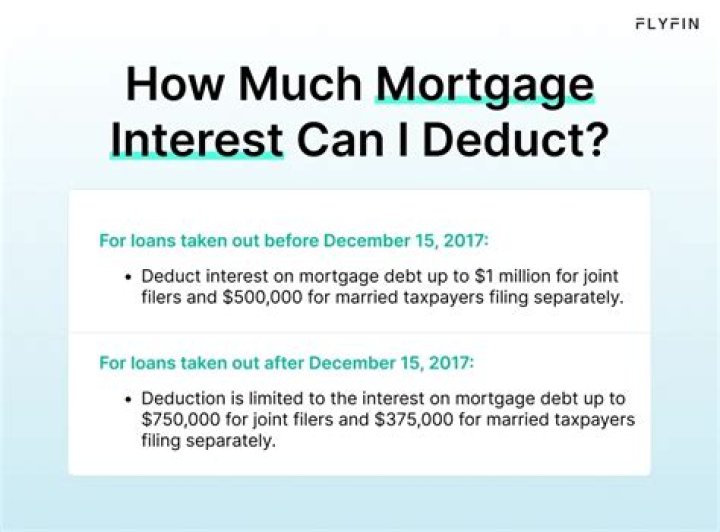

Generally, the Internal Revenue Service (IRS) allows you to deduct the full amount of your points in the year you pay them. If the amount you borrow to buy your home exceeds $750,000 million ($1M for mortgages originated before December 15, 2017), you are generally limited on the amount of points that you can deduct.

Also, is mortgage interest deductible for 2018? The mortgage interest deduction is one of them. Starting in 2018, mortgage interest on total principal of as much as $750,000 in qualified residence loans can be deducted, down from the previous principal limit of $1,000,000. It's worth pointing out that this limit only applies to new loans originated after 2017.

Similarly, it is asked, how can I tell if I paid points on my mortgage?

If you have points, they should be listed in Box 6 of your Form 1098, Mortgage Interest Statement. If you have your closing documents, you can do the following: Locate the “Settlement Statement” in the closing documents. The name should be clearly defined at the top of the document.

Is mortgage interest still tax deductible?

Taxpayers can deduct the interest paid on first and second mortgages up to $1,000,000 in mortgage debt (the limit is $500,000 if married and filing separately). Any interest paid on first or second mortgages over this amount is not tax deductible. The most common mortgage terms are 15 years and 30 years.

Related Question AnswersIs paying points on a mortgage worth it?

Paying mortgage points to get a lower rate on a mortgage is almost always a losing proposition. Most homeowners don't keep their mortgages long enough to do more than recoup the up-front cost of paying points. A point is 1% of your loan amount. If you take out a $250,000 mortgage, 1 point equals $2,500.What mortgage costs are tax deductible?

3. Are mortgage closing costs tax deductible? In general, the only settlement or closing costs you can deduct are home mortgage interest and certain real estate taxes. You deduct them in the year you buy your home if you itemize your deductions.Is prepaid mortgage interest tax deductible?

You can deduct in each year only the interest that qualifies as home mortgage interest for that year. You can fully deduct prepaid mortgage interest points in the year you paid them if you meet all of these tests: Your loan is secured by your main home (not a second home).Can you write off mortgage insurance in 2019?

It is totally removed once you go over $109,000 per year AGI. Depending upon the level of your adjusted gross income, you may be able to deduct mortgage insurance for FHA and USDA loans as well. It's no wonder why we are receiving so many emails asking whether mortgage insurance and PMI is tax deductible in 2018.Is it smart to buy points on a mortgage?

Should you buy mortgage points? If you're buying a home, you can to purchase "discount" points to lower your interest rate — but you could also use that cash to make a larger down payment. Lenders typically decrease your interest rate by a quarter of a percentage point for every point you buy, up to a limit.Is MIP tax deductible 2019?

PMI, along with other eligible forms of mortgage insurance premiums, was tax deductible only through the 2017 tax year as an itemized deduction. That means it's available for the 2019 and 2020 tax years, and retroactively for 2018 taxes, too.How does new tax law affect mortgage interest?

Under the new tax law, homeowners can only deduct mortgage interest paid on up to $750,000 on a first or second home. This new law only applies to homes purchased after Dec. 15, 2017. Purchasing a new home at a comparable purchase price may reduce the amount of mortgage interest you're able to deduct.What percentage of interest on mortgage is tax deductible?

A taxpayer spending $12,000 on mortgage interest and paying taxes at an individual income tax rate of 35% would receive only a $4,200 tax deduction. That's slightly less than what the taxpayer would receive from taking the standard deduction.What do mortgage points mean on taxes?

Mortgage points, also known as discount points, are fees paid directly to the lender at closing in exchange for a reduced interest rate. This is also called “buying down the rate,” which can lower your monthly mortgage payments. One point costs 1 percent of your mortgage amount (or $1,000 for every $100,000).Do you get a tax credit for refinancing your home?

Refinancing your home mortgage at a lower interest rate can save you a significant amount of money each month. However, you can also save some money on your taxes by deducting some of the costs you incur during the refinance. Deductible costs include mortgage interest, points and property taxes paid at closing.What is the advantage of buying points on a mortgage?

Mortgage points, or discount points, are fees you pay your lender at closing in exchange for a better interest rate. This can lower your monthly mortgage payments and is also known as “buying down the rate.” One point costs 1% of the total loan amount.Can I deduct origination fees on my taxes?

Deducting Home Loan Origination Fees. You can deduct mortgage interest— such as home loan origination fees, maximum loan charges, and loan discounts— through the point system. Points you pay (and even points the seller pays) when you purchase your home are generally tax deductible in full the year you pay them.How can I lower my mortgage APR?

10 Ways to Lower Your Mortgage Rate- Maintain a good credit score.

- Have a long and consistent work history.

- Shop around for the best rate.

- Ask your bank/credit union for a better rate.

- Put more money down.

- Shorten your loan.

- Consider the adjustable-rate vs. fixed-rate loan trade-off.

- Pay for points.