Can I use home equity line of credit to buy another house?

.

Herein, should I use a Heloc to buy a second home?

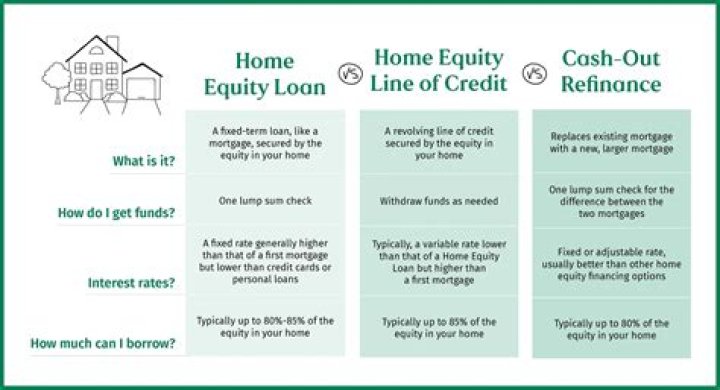

A HELOC is a great option for short-term cash needs, especially if you're going to pay it off quickly. But if you're using a HELOC to buy a home — which you can do by having a HELOC be a second mortgage — and you don't intend to pay it off quickly, you may want to consider a fixed-rate second mortgage.

Secondly, can you use equity in a home as a down payment? You can accomplish this through home equity line of credit or a home equity loan. When using home equity loan or HELOC for a down payment on a new home, the idea is to pay it off in full once you sell the property. If you don't use all your credit, you don't have to repay it.

Also know, how do you use equity to buy another property?

Take out a line of credit. Another way to unlock equity is through a home equity or line of credit loan. This is a separate home loan that extends you an amount of credit based on the equity in your property. You can use as much or as little of the credit limit as you like, and only pay interest on the amount you use.

Can you use a Heloc as a downpayment on a second home?

You can take out a home equity loan (HEL) or home equity line of credit (HELOC) to make the down payment on your second home. Your first home serves as collateral. Advantages of HELs and HELOCs as a down payment include the following: You may be able to deduct the interest paid on home equity debt, up to $100,000.

Related Question AnswersWhat happens if you don't use a Heloc?

If you don't, the lender will foreclose. Even if you have a HELOC that only charges interest on the outstanding debt during the first 10 years, the loan will go into repayment mode after that, requiring you to pay both principal and interest.Can I borrow money against my house to buy another property?

Yes, remortgaging one property to release equity that is used to help buy another property is a common method that landlords use to grow their portfolio. Some buy to let lenders will lend up to a maximum loan to value of 85% and affordability is based on the level of rental income that can be achieved by the property.How do you pay back a Heloc?

Home equity loans are paid back via fixed monthly payments at a fixed interest rate. HELOCs allow you to make interest-only payments during the draw period, then you make principal and interest payments after.What happens to a Heloc when you sell your house?

Normally, you can sell your home without obtaining mortgage or HELOC lien holder permission as long as those lenders are paid off at sale closing. Your home's lien holders will be paid from your home's sale proceeds before you, in other words.Can I buy a second home and rent the first?

All you have to do is move out and stick a “For Rent” sign in the yard. Getting a mortgage for a second home is just like the process you went through to buy your first home. Approval depends on your income, savings, down payment, credit rating, and debt-to-income ratios.Can you use a Heloc for anything?

Like a home equity loan, a HELOC can be used for anything you want. However, it's best-suited for long-term, ongoing expenses like home renovations, medical bills or even college tuition. A HELOC usually has a variable interest rate based on the fluctuations of an index, such as the prime rate.How does a Heloc affect your credit?

Because it has a minimum monthly payment and a limit, a HELOC can directly affect your credit score since it looks like a credit card to credit agencies. Since a HELOC has a variable interest rate, payments can increase when interest rates rise and decrease when interest rates fall.How much deposit do I need for a second house?

Many second home mortgages require at least a 25% deposit, and you may need even more than that if your current income won't cover both mortgages at the same time. In addition to this, your income will be even more important in the application for a second home mortgage.How much equity do you need to buy another house?

Let's say the market value of your existing home is $500,000 and the balance of your mortgage is $300,000. The difference between the two is $200,000, which is your home equity. As an investor you can access up to 80% of your home equity (without the need to take out LMI), which equates to $160,000 in this example.Does using equity increase repayments?

Larger repayments Accessing equity is done via increasing how much you owe. It is still a loan with interest charged for using the funds. At the moment, you may be able to afford your current repayments, however, if you increase your home loan your repayments will increase.How can I buy a second home with no deposit?

How do I buy a second property with no deposit?- You can generally release up to 80-90% of the value in your property in equity to buy a second property.

- You must owe less than 80% of the property value on your home loan.

- Your mortgage repayment history must be perfect.

- You'll need to provide your last two payslips.